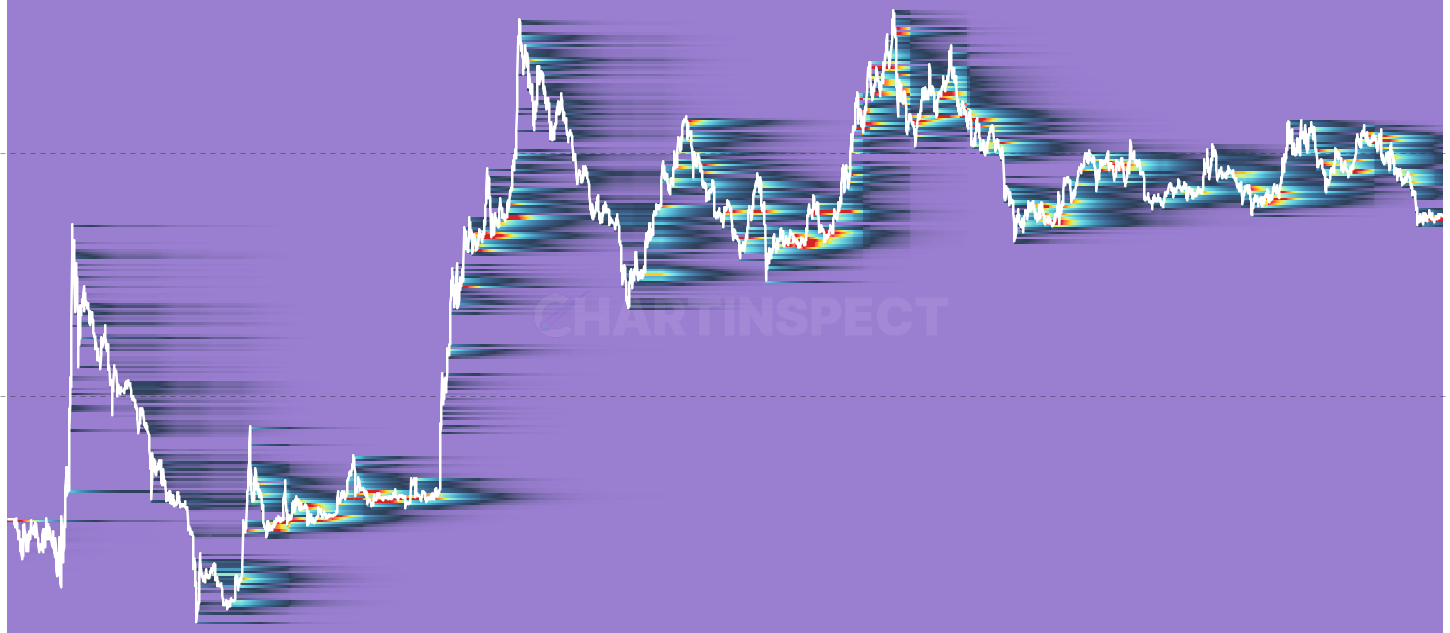

SOPR Volatility Ratio: Bitcoin On-Chain Indicator

SOPR Volatility Ratio reveals when profit-taking or loss-realization is truly extreme relative to typical market behavior, normalizing SOPR by its own volatility. This makes readings comparable across different volatility regimes.

What is SOPR Volatility Ratio?

SOPR Volatility Ratio is a Bitcoin on-chain indicator categorized under SOPR Analysis. SOPR Volatility Ratio reveals when profit-taking or loss-realization is truly extreme relative to typical market behavior, normalizing SOPR by its own volatility. This makes readings comparable across different volatility regimes.

How to read SOPR Volatility Ratio

Use this chart to identify Bitcoin on-chain regime shifts: zoom into specific cycles, compare the indicator against price, and watch for extreme readings that historically marked turning points. Toggle the timeframe selector for short-term tactical reads (30d, 90d, 1y) or full-history macro context.

Related On-Chain Metrics charts

- Realized Cap / Gold Ratio: Compares Bitcoin's Realized Cap (aggregate cost basis of all coins) to the gold price

- Composite Momentum: Combines multiple on-chain momentum indicators into composite metrics: Binary Consensus (% of indicators bullish) and Weighted Momentum Score

- Active MVRV Norm: Active MVRV adjusted for network activity using Cointime Economics principles, then normalized over a multi-cycle rolling window to produce a consistent 0-100% cycle indicator

- Crypto Risk Metrics: Monitor cryptocurrency market risk indicators and volatility

- Adaptive Risk Oscillator: Advanced risk metric using autocorrelation, variance decay, entropy, and fractal analysis to create a dynamic oscillator

Exhibits6

Cryptocurrency931

Alpha (Momentum/Deviation)PRO

Cryptocurrency Market BreadthPRO

Altcoin Season IndexPRO

Combined VWAP MVRV Z-ScorePRO

Advanced Decline IndexPRO

Fear & Greed Index

Price Horizons

ROI Analysis

Sharpe Ratio Analysis

RSI

Economic Indicators vs Crypto Correlation

Global M2 vs Crypto Correlation

GoldWave

Death Cross Analysis

Monthly Returns Table

Days Since Percentage Decline

Price Derivative

OG Whale Spending EventsPRO

Cumulative LTH Realized Profit [Bull Market]PRO

STH vs LTH Supply

Cohort Supply P/L

Hodler Net Position Change

LTH Wealth Concentration

LTH Wealth Concentration AttributionNEW

STH Wealth Concentration

STH % Supply in Profit

STH % Supply in Loss

LTH % Supply in Profit

LTH % Supply in Loss

Active Supply in Profit & Loss

Vaulted Supply in Profit & Loss

STH Net Position Change

LTH Net Position Change

Realized P&L By Age

Revived Supply By Age

Supply Last Active 1yr+ Net Position Change

Percent of Supply Last Active 1yr+NEW

Apparent Demand

LTH Maturation vs Distribution

Forward-Looking LTH Accumulation

NUPL by Cohort RiskPRO

Relative Unrealized P/LPRO

STH/LTH Profit-to-Volatility RatioPRO

STH/LTH CDDPRONEW

Relative Unrealized P/L by CohortPRONEW

Relative Unrealized P/L by AgePRONEW

Supply In Profit/Loss

NUPL

NUPL Z-Score

aSOPR

STH-NUPL

LTH-NUPL

AVIV-NUPL

SOPR

RHODL Ratio

STH/LTH Realized Price Ratio

Market Realized P/L Ratio

SLRV Ratio

Bull Market SOPR Loss Pressure

Cost Basis Heatmaps1

Unrealized P/L Heatmaps1

Address Count Heatmaps1

Market Cap by AgePRONEW

Balance Distribution (Shrimp to Whale)PRO

Balance Distribution Flows (Whale Accumulation)PRO

Accumulation IndexPRO

Whale vs Retail Delta HeatmapPRO

Accumulation WavesPRO

HODL Waves in Profit/LossPRONEW

Cost Basis QuantilesPRONEW

Realized Cap HODL Profit/LossPRONEW

Yearly Absorption RatePRONEW

HODL Waves

UTXO Realized Price Distribution

URPD by Age Cohort

Daily Issuance

Block Rewards

Circulating Supply

Cost Basis Heatmaps3

Unrealized P/L Heatmaps3

Realized P/L Heatmaps4

Address Count Heatmaps3

SOPD Heatmaps4

Cross-Chain AnalyticsPRO

Price vs MVRV Percentile Divergence MomentumPRO

Onchain Risk CompositePRO

Realized P/L by BandPRONEW

Cost Basis ConcentrationPRONEW

Implied On-Chain VolatilityPRONEW

CB Profit/Loss RatioPRONEW

CB Profit Take RatePRONEW

CB Supply ShiftPRONEW

Bitcoin Cycle Index (BCI)PRO

Cost Basis ConvergencePRO

Seller Exhaustion ConstantPRO

Cost Basis Distribution by Age CohortPRONEW

Median Cost Basis by Age CohortPRONEW

STH Median MVRVPRONEW

LTH Median MVRVPRONEW

STH:LTH Median Cost Basis RatioPRONEW

Seller Median Cost BasisPRONEW

LTH Adaptive MVRV Z-Score

Price vs MVRV Percentile Divergence

Sell Side Pressure

Realized P&L Sharpe Ratio

Realized P&L Acceleration

UTXO Entropy Cascade

ETH STH vs LTH SupplyPRO

ETH Hodler Net Position ChangePRO

ETH STH-SOPRPRO

ETH LTH-SOPRPRO

ETH SOPR by AgePRO

ETH OG Whale Spending EventsPRO

ETH SOPR Z-ScorePRO

ETH STH Cost BasisPRO

ETH STH Cost Basis ChangePRO

ETH LTH Wealth ConcentrationPRO

ETH Cumulative LTH Realized Profit [Bull Market]PRO

ETH STH Wealth ConcentrationPRO

ETH STH % Supply in ProfitPRO

ETH STH % Supply in LossPRO

ETH LTH % Supply in ProfitPRO

ETH LTH % Supply in LossPRO

ETH Active Supply in Profit & LossPRO

ETH Vaulted Supply in Profit & LossPRO

ETH STH Net Position ChangePRO

ETH LTH Net Position ChangePRO

ETH LTH Cost BasisPRO

ETH LTH Cost Basis ChangePRO

ETH STH MVRVPRO

ETH LTH MVRVPRO

ETH Holder Realized PricesPRO

ETH STH StressPRO

ETH LTH StressPRO

ETH STH MVRV Z-ScorePRO

ETH LTH MVRV Z-ScorePRO

ETH Realized P&L DeviationPRO

ETH SOPR by Cost Basis BandPRONEW

ETH Realized P&L By AgePRO

ETH Revived Supply By AgePRO

ETH Supply Last Active 1yr+ Net Position ChangePRO

ETH Percent of Supply Last Active 1yr+PRONEW

ETH LTH Realized P/L RatioPRO

ETH STH Realized P/L RatioPRO

ETH STH P/L Price FlowPRO

ETH LTH P/L Price FlowPRO

ETH Relative Long/Short-Term Holder Realized P/LPRO

ETH Active MVRV NormPRO

ETH CVDD BandsPRO

ETH MVRVPRO

ETH True Market Mean AVIVPRO

ETH Onchain Price LevelsPRO

ETH Realized P&LPRO

ETH Net Realized P&LPRO

ETH Relative Realized P/LPRO

ETH MVRV BandsPRO

ETH Reserve RiskPRO

ETH Reserve Risk AdjustedPRO

ETH MVRV Z-ScorePRO

ETH Median MVRVPRONEW

ETH Realized CapPRO

ETH Realized Cap DrawdownPRO

ETH Days Above/Below Realized PricePRO

ETH Sell-Side Risk RatioPRO

ETH Vaultedness - Active MVRV DivergencePRO

ETH Market Cap to Thermocap Ratio (MCTC)PRO

ETH AVIV Z-ScorePRO

ETH AVIV BandsPRO

ETH Active MVRV & Active Realized PricePRO

ETH Puell MultiplePRO

ETH Investorness & ProducernessPRO

ETH HODL WavesPRO

ETH Market Cap by AgePRONEW

ETH Balance Distribution (Shrimp to Whale)PRO

ETH Accumulation IndexPRO

ETH Whale vs Retail Delta HeatmapPRO

ETH Cost Basis HeatmapPRONEW

ETH HODL Waves in Profit/LossPRONEW

ETH Cost Basis QuantilesPRONEW

ETH Unrealized P/L HeatmapPRONEW

ETH Realized Cap HODL Profit/LossPRONEW

ETH Address Count HeatmapPRONEW

ETH Daily IssuancePRO

ETH Circulating SupplyPRO

ETH LTH Adaptive MVRV Z-ScorePRO

ETH Onchain Risk CompositePRO

ETH Sell Side PressurePRO

ETH Realized P/L by BandPRONEW

ETH Realized P/L HeatmapPRONEW

ETH Cost Basis ConcentrationPRONEW

ETH Implied On-Chain VolatilityPRONEW

ETH CB Profit/Loss RatioPRONEW

ETH CB Profit Take RatePRONEW

ETH CB Supply ShiftPRONEW

ETH Realized P&L Sharpe RatioPRO

ETH Cost Basis ConvergencePRO

ETH Realized P&L AccelerationPRO

ETH Seller Exhaustion ConstantPRO

ETH SOPD HeatmapPRONEW

ETH STH Cost Basis DistributionPRONEW

ETH LTH Cost Basis DistributionPRONEW

ETH STH Unrealized P/L HeatmapPRONEW

ETH LTH Unrealized P/L HeatmapPRONEW

ETH STH Address Count HeatmapPRONEW

ETH LTH Address Count HeatmapPRONEW

ETH STH SOPD HeatmapPRONEW

ETH LTH SOPD HeatmapPRONEW

ETH STH Realized P/L HeatmapPRONEW

ETH LTH Realized P/L HeatmapPRONEW

ETH Cost Basis Heatmap by Age CohortPRONEW

ETH Cost Basis Distribution by Age CohortPRONEW

ETH Unrealized P/L Heatmap by Age CohortPRONEW

ETH Address Count Heatmap by Age CohortPRONEW

ETH SOPD Heatmap by Age CohortPRONEW

ETH Realized P/L Heatmap by Age CohortPRONEW

ETH Median Cost Basis by Age CohortPRONEW

ETH STH Median MVRVPRONEW

ETH LTH Median MVRVPRONEW

ETH STH:LTH Median Cost Basis RatioPRONEW

ETH Seller Median Cost BasisPRONEW

DOGE STH vs LTH SupplyPRO

DOGE Hodler Net Position ChangePRO

DOGE STH-SOPRPRO

DOGE LTH-SOPRPRO

DOGE SOPR by AgePRO

DOGE SOPR Z-ScorePRO

DOGE STH Cost BasisPRO

DOGE STH Cost Basis ChangePRO

DOGE LTH Wealth ConcentrationPRO

DOGE STH Wealth ConcentrationPRO

DOGE STH % Supply in ProfitPRO

DOGE STH % Supply in LossPRO

DOGE LTH % Supply in ProfitPRO

DOGE LTH % Supply in LossPRO

DOGE Active Supply in Profit & LossPRO

DOGE Vaulted Supply in Profit & LossPRO

DOGE STH Net Position ChangePRO

DOGE LTH Net Position ChangePRO

DOGE LTH Cost BasisPRO

DOGE LTH Cost Basis ChangePRO

DOGE STH MVRVPRO

DOGE LTH MVRVPRO

DOGE Holder Realized PricesPRO

DOGE STH StressPRO

DOGE LTH StressPRO

DOGE STH MVRV Z-ScorePRO

DOGE LTH MVRV Z-ScorePRO

DOGE Realized P&L DeviationPRO

DOGE SOPR by Cost Basis BandPRONEW

DOGE Realized P&L By AgePRO

DOGE Revived Supply By AgePRO

DOGE Supply Last Active 1yr+ Net Position ChangePRO

DOGE Percent of Supply Last Active 1yr+PRONEW

DOGE LTH Realized P/L RatioPRO

DOGE STH Realized P/L RatioPRO

DOGE STH P/L Price FlowPRO

DOGE LTH P/L Price FlowPRO

DOGE Relative Long/Short-Term Holder Realized P/LPRO

DOGE Active MVRV NormPRO

DOGE CVDD BandsPRO

DOGE MVRVPRO

DOGE True Market Mean AVIVPRO

DOGE Onchain Price LevelsPRO

DOGE Realized P&LPRO

DOGE Net Realized P&LPRO

DOGE Relative Realized P/LPRO

DOGE MVRV BandsPRO

DOGE Reserve RiskPRO

DOGE Reserve Risk AdjustedPRO

DOGE MVRV Z-ScorePRO

DOGE Median MVRVPRONEW

DOGE Realized CapPRO

DOGE Realized Cap DrawdownPRO

DOGE Days Above/Below Realized PricePRO

DOGE Sell-Side Risk RatioPRO

DOGE Vaultedness - Active MVRV DivergencePRO

DOGE Market Cap to Thermocap Ratio (MCTC)PRO

DOGE AVIV Z-ScorePRO

DOGE AVIV BandsPRO

DOGE Active MVRV & Active Realized PricePRO

DOGE Puell MultiplePRO

DOGE Investorness & ProducernessPRO

DOGE Supply In Profit/LossPRO

DOGE NUPLPRO

DOGE NUPL Z-ScorePRO

DOGE Relative Unrealized P/LPRO

DOGE aSOPRPRO

DOGE STH-NUPLPRO

DOGE LTH-NUPLPRO

DOGE AVIV-NUPLPRO

DOGE SOPRPRO

DOGE RHODL RatioPRO

DOGE STH/LTH Realized Price RatioPRO

DOGE Market Realized P/L RatioPRO

DOGE SLRV RatioPRO

DOGE STH/LTH CDDPRONEW

DOGE Active AddressesPRONEW

DOGE Composite MomentumPRO

DOGE STH-NUPL MomentumPRO

DOGE LTH-NUPL MomentumPRO

DOGE Realized P&L Deviation MomentumPRO

DOGE RHODL MomentumPRO

DOGE LTH Realized P/L Ratio MomentumPRO

DOGE STH Realized P/L Ratio MomentumPRO

DOGE MVRV MomentumPRO

DOGE AVIV MomentumPRO

DOGE STH SOPR MomentumPRO

DOGE LTH SOPR MomentumPRO

DOGE VDD MultiplePRO

DOGE Block HeightPRO

DOGE Thermocap FlowPRO

DOGE CDD (Coin Days Dest.)PRO

DOGE Daily UTXOs SpentPRO

DOGE Daily UTXOs CreatedPRO

DOGE Transaction FeesPRO

DOGE Blocks MinedPRO

DOGE Coinblocks CreatedPRO

DOGE Coinblocks DestroyedPRO

DOGE LivelinessPRO

DOGE VaultednessPRO

DOGE A2VR - Activity to Vaulted RatioPRO

DOGE A2VR MomentumPRO

DOGE LTH Adaptive MVRV Z-ScorePRO

DOGE Onchain Risk CompositePRO

DOGE Sell Side PressurePRO

DOGE Realized P/L by BandPRONEW

DOGE Realized P/L HeatmapPRONEW

DOGE Cost Basis ConcentrationPRONEW

DOGE Implied On-Chain VolatilityPRONEW

DOGE CB Profit/Loss RatioPRONEW

DOGE CB Profit Take RatePRONEW

DOGE CB Supply ShiftPRONEW

DOGE Realized P&L Sharpe RatioPRO

DOGE Cost Basis ConvergencePRO

DOGE Realized P&L AccelerationPRO

DOGE Seller Exhaustion ConstantPRO

DOGE SOPD HeatmapPRONEW

DOGE STH Cost Basis DistributionPRONEW

DOGE LTH Cost Basis DistributionPRONEW

DOGE STH Unrealized P/L HeatmapPRONEW

DOGE LTH Unrealized P/L HeatmapPRONEW

DOGE STH Address Count HeatmapPRONEW

DOGE LTH Address Count HeatmapPRONEW

DOGE STH SOPD HeatmapPRONEW

DOGE LTH SOPD HeatmapPRONEW

DOGE STH Realized P/L HeatmapPRONEW

DOGE LTH Realized P/L HeatmapPRONEW

DOGE Cost Basis Heatmap by Age CohortPRONEW

DOGE Cost Basis Distribution by Age CohortPRONEW

DOGE Unrealized P/L Heatmap by Age CohortPRONEW

DOGE Address Count Heatmap by Age CohortPRONEW

DOGE SOPD Heatmap by Age CohortPRONEW

DOGE Realized P/L Heatmap by Age CohortPRONEW

DOGE Median Cost Basis by Age CohortPRONEW

DOGE STH Median MVRVPRONEW

DOGE LTH Median MVRVPRONEW

DOGE STH:LTH Median Cost Basis RatioPRONEW

DOGE Seller Median Cost BasisPRONEW

LTC STH vs LTH SupplyPRO

LTC Hodler Net Position ChangePRO

LTC STH-SOPRPRO

LTC LTH-SOPRPRO

LTC SOPR by AgePRO

LTC SOPR Z-ScorePRO

LTC STH Cost BasisPRO

LTC STH Cost Basis ChangePRO

LTC LTH Wealth ConcentrationPRO

LTC STH Wealth ConcentrationPRO

LTC STH % Supply in ProfitPRO

LTC STH % Supply in LossPRO

LTC LTH % Supply in ProfitPRO

LTC LTH % Supply in LossPRO

LTC Active Supply in Profit & LossPRO

LTC Vaulted Supply in Profit & LossPRO

LTC STH Net Position ChangePRO

LTC LTH Net Position ChangePRO

LTC LTH Cost BasisPRO

LTC LTH Cost Basis ChangePRO

LTC STH MVRVPRO

LTC LTH MVRVPRO

LTC Holder Realized PricesPRO

LTC STH StressPRO

LTC LTH StressPRO

LTC STH MVRV Z-ScorePRO

LTC LTH MVRV Z-ScorePRO

LTC Realized P&L DeviationPRO

LTC SOPR by Cost Basis BandPRONEW

LTC Realized P&L By AgePRO

LTC Revived Supply By AgePRO

LTC Supply Last Active 1yr+ Net Position ChangePRO

LTC Percent of Supply Last Active 1yr+PRONEW

LTC LTH Realized P/L RatioPRO

LTC STH Realized P/L RatioPRO

LTC STH P/L Price FlowPRO

LTC LTH P/L Price FlowPRO

LTC Relative Long/Short-Term Holder Realized P/LPRO

LTC Active MVRV NormPRO

LTC CVDD BandsPRO

LTC MVRVPRO

LTC True Market Mean AVIVPRO

LTC Onchain Price LevelsPRO

LTC Realized P&LPRO

LTC Net Realized P&LPRO

LTC Relative Realized P/LPRO

LTC MVRV BandsPRO

LTC Reserve RiskPRO

LTC Reserve Risk AdjustedPRO

LTC MVRV Z-ScorePRO

LTC Median MVRVPRONEW

LTC Realized CapPRO

LTC Realized Cap DrawdownPRO

LTC Days Above/Below Realized PricePRO

LTC Sell-Side Risk RatioPRO

LTC Market Cap to Thermocap Ratio (MCTC)PRO

LTC AVIV Z-ScorePRO

LTC AVIV BandsPRO

LTC Active MVRV & Active Realized PricePRO

LTC Puell MultiplePRO

LTC Investorness & ProducernessPRO

LTC Supply In Profit/LossPRO

LTC NUPLPRO

LTC NUPL Z-ScorePRO

LTC Relative Unrealized P/LPRO

LTC aSOPRPRO

LTC STH-NUPLPRO

LTC LTH-NUPLPRO

LTC AVIV-NUPLPRO

LTC SOPRPRO

LTC RHODL RatioPRO

LTC STH/LTH Realized Price RatioPRO

LTC Market Realized P/L RatioPRO

LTC SLRV RatioPRO

LTC STH/LTH CDDPRONEW

LTC Active/Vaulted Profit & LossPRONEW

LTC Active AddressesPRONEW

LTC VDD MultiplePRO

LTC Block HeightPRO

LTC Thermocap FlowPRO

LTC CDD (Coin Days Dest.)PRO

LTC ACDD (Adjusted CDD)PRO

LTC Transaction FeesPRO

LTC Hash RatePRO

LTC Blocks MinedPRO

LTC Coinblocks CreatedPRO

LTC Coinblocks DestroyedPRO

LTC LivelinessPRO

LTC VaultednessPRO

LTC A2VR - Activity to Vaulted RatioPRO

LTC A2VR MomentumPRO

LTC LTH Adaptive MVRV Z-ScorePRO

LTC Onchain Risk CompositePRO

LTC Sell Side PressurePRO

LTC Realized P/L by BandPRONEW

LTC Realized P/L HeatmapPRONEW

LTC Cost Basis ConcentrationPRONEW

LTC Implied On-Chain VolatilityPRONEW

LTC CB Profit/Loss RatioPRONEW

LTC CB Profit Take RatePRONEW

LTC CB Supply ShiftPRONEW

LTC Realized P&L Sharpe RatioPRO

LTC Cost Basis ConvergencePRO

LTC Realized P&L AccelerationPRO

LTC Seller Exhaustion ConstantPRO

LTC SOPD HeatmapPRONEW

LTC STH Cost Basis DistributionPRONEW

LTC LTH Cost Basis DistributionPRONEW

LTC STH Unrealized P/L HeatmapPRONEW

LTC LTH Unrealized P/L HeatmapPRONEW

LTC STH Address Count HeatmapPRONEW

LTC LTH Address Count HeatmapPRONEW

LTC STH SOPD HeatmapPRONEW

LTC LTH SOPD HeatmapPRONEW

LTC STH Realized P/L HeatmapPRONEW

LTC LTH Realized P/L HeatmapPRONEW

LTC Cost Basis Heatmap by Age CohortPRONEW

LTC Cost Basis Distribution by Age CohortPRONEW

LTC Unrealized P/L Heatmap by Age CohortPRONEW

LTC Address Count Heatmap by Age CohortPRONEW

LTC SOPD Heatmap by Age CohortPRONEW

LTC Realized P/L Heatmap by Age CohortPRONEW

LTC Median Cost Basis by Age CohortPRONEW

LTC STH Median MVRVPRONEW

LTC LTH Median MVRVPRONEW

LTC STH:LTH Median Cost Basis RatioPRONEW

LTC Seller Median Cost BasisPRONEW

ADA STH vs LTH SupplyPRO

ADA Hodler Net Position ChangePRO

ADA STH-SOPRPRO

ADA LTH-SOPRPRO

ADA SOPR by AgePRO

ADA SOPR Z-ScorePRO

ADA STH Cost BasisPRO

ADA STH Cost Basis ChangePRO

ADA LTH Wealth ConcentrationPRO

ADA STH Wealth ConcentrationPRO

ADA STH % Supply in ProfitPRO

ADA STH % Supply in LossPRO

ADA LTH % Supply in ProfitPRO

ADA LTH % Supply in LossPRO

ADA Active Supply in Profit & LossPRO

ADA Vaulted Supply in Profit & LossPRO

ADA STH Net Position ChangePRO

ADA LTH Net Position ChangePRO

ADA LTH Cost BasisPRO

ADA LTH Cost Basis ChangePRO

ADA STH MVRVPRO

ADA LTH MVRVPRO

ADA Holder Realized PricesPRO

ADA STH StressPRO

ADA LTH StressPRO

ADA STH MVRV Z-ScorePRO

ADA LTH MVRV Z-ScorePRO

ADA Realized P&L DeviationPRO

ADA SOPR by Cost Basis BandPRONEW

ADA Realized P&L By AgePRO

ADA Revived Supply By AgePRO

ADA Supply Last Active 1yr+ Net Position ChangePRO

ADA Percent of Supply Last Active 1yr+PRONEW

ADA LTH Realized P/L RatioPRO

ADA STH Realized P/L RatioPRO

ADA STH P/L Price FlowPRO

ADA LTH P/L Price FlowPRO

ADA Active MVRV NormPRO

ADA CVDD BandsPRO

ADA MVRVPRO

ADA True Market Mean AVIVPRO

ADA Onchain Price LevelsPRO

ADA Realized P&LPRO

ADA Net Realized P&LPRO

ADA Relative Realized P/LPRO

ADA MVRV BandsPRO

ADA Reserve RiskPRO

ADA Reserve Risk AdjustedPRO

ADA MVRV Z-ScorePRO

ADA Median MVRVPRONEW

ADA Realized CapPRO

ADA Realized Cap DrawdownPRO

ADA Days Above/Below Realized PricePRO

ADA Sell-Side Risk RatioPRO

ADA Market Cap to Thermocap Ratio (MCTC)PRO

ADA AVIV Z-ScorePRO

ADA AVIV BandsPRO

ADA Active MVRV & Active Realized PricePRO

ADA Puell MultiplePRO

ADA Investorness & ProducernessPRO

ADA LTH Adaptive MVRV Z-ScorePRO

ADA Onchain Risk CompositePRO

ADA Sell Side PressurePRO

ADA Realized P/L by BandPRONEW

ADA Realized P/L HeatmapPRONEW

ADA Cost Basis ConcentrationPRONEW

ADA Implied On-Chain VolatilityPRONEW

ADA CB Profit/Loss RatioPRONEW

ADA CB Profit Take RatePRONEW

ADA CB Supply ShiftPRONEW

ADA Realized P&L Sharpe RatioPRO

ADA Cost Basis ConvergencePRO

ADA Realized P&L AccelerationPRO

ADA Seller Exhaustion ConstantPRO

ADA SOPD HeatmapPRONEW

ADA STH Cost Basis DistributionPRONEW

ADA LTH Cost Basis DistributionPRONEW

ADA STH Unrealized P/L HeatmapPRONEW

ADA LTH Unrealized P/L HeatmapPRONEW

ADA STH Address Count HeatmapPRONEW

ADA LTH Address Count HeatmapPRONEW

ADA STH SOPD HeatmapPRONEW

ADA LTH SOPD HeatmapPRONEW

ADA STH Realized P/L HeatmapPRONEW

ADA LTH Realized P/L HeatmapPRONEW

ADA Cost Basis Heatmap by Age CohortPRONEW

ADA Cost Basis Distribution by Age CohortPRONEW

ADA Unrealized P/L Heatmap by Age CohortPRONEW

ADA Address Count Heatmap by Age CohortPRONEW

ADA SOPD Heatmap by Age CohortPRONEW

ADA Realized P/L Heatmap by Age CohortPRONEW

ADA Median Cost Basis by Age CohortPRONEW

ADA STH Median MVRVPRONEW

ADA LTH Median MVRVPRONEW

ADA STH:LTH Median Cost Basis RatioPRONEW

ADA Seller Median Cost BasisPRONEW

LINK STH vs LTH SupplyPRO

LINK Hodler Net Position ChangePRO

LINK STH-SOPRPRO

LINK LTH-SOPRPRO

LINK SOPR by AgePRO

LINK OG Whale Spending EventsPRO

LINK SOPR Z-ScorePRO

LINK STH Cost BasisPRO

LINK STH Cost Basis ChangePRO

LINK LTH Wealth ConcentrationPRO

LINK STH Wealth ConcentrationPRO

LINK STH % Supply in ProfitPRO

LINK STH % Supply in LossPRO

LINK LTH % Supply in ProfitPRO

LINK LTH % Supply in LossPRO

LINK STH Net Position ChangePRO

LINK LTH Net Position ChangePRO

LINK LTH Cost BasisPRO

LINK LTH Cost Basis ChangePRO

LINK STH MVRVPRO

LINK LTH MVRVPRO

LINK Holder Realized PricesPRO

LINK STH StressPRO

LINK LTH StressPRO

LINK STH MVRV Z-ScorePRO

LINK LTH MVRV Z-ScorePRO

LINK Realized P&L DeviationPRO

LINK SOPR by Cost Basis BandPRONEW

LINK Realized P&L By AgePRO

LINK Revived Supply By AgePRO

LINK Supply Last Active 1yr+ Net Position ChangePRO

LINK Percent of Supply Last Active 1yr+PRONEW

LINK STH P/L Price FlowPRO

LINK LTH P/L Price FlowPRO

LINK Relative Long/Short-Term Holder Realized P/LPRO

LINK HODL WavesPRO

LINK Market Cap by AgePRONEW

LINK Balance Distribution (Shrimp to Whale)PRO

LINK Accumulation IndexPRO

LINK Whale vs Retail Delta HeatmapPRO

LINK Cost Basis HeatmapPRONEW

LINK HODL Waves in Profit/LossPRONEW

LINK Cost Basis QuantilesPRONEW

LINK Unrealized P/L HeatmapPRONEW

LINK Realized Cap HODL Profit/LossPRONEW

LINK Address Count HeatmapPRONEW

LINK Circulating SupplyPRO

LINK LTH Adaptive MVRV Z-ScorePRO

LINK Onchain Risk CompositePRO

LINK Sell Side PressurePRO

LINK Realized P/L by BandPRONEW

LINK Realized P/L HeatmapPRONEW

LINK Cost Basis ConcentrationPRONEW

LINK Implied On-Chain VolatilityPRONEW

LINK Realized P&L Sharpe RatioPRO

LINK Cost Basis ConvergencePRO

LINK Realized P&L AccelerationPRO

LINK Seller Exhaustion ConstantPRO

Economics30

Dashboards3

Crypto Risk Metrics

PROCrypto Risk · Monitor cryptocurrency market risk indicators and volatility

B

B

E

E

A

A

Adaptive Risk Oscillator

PROCrypto Risk · Advanced risk metric using autocorrelation, variance decay, ...

B

B

E

E

A

A

Risk Values Non Color Coded

PROCrypto Risk · Analyze cryptocurrency risk values with traditional line cha...

B

B

E

E

A

A

Crypto Market Risk Indicator

PROCrypto Risk · Aggregate risk levels from top cryptocurrencies into a singl...

B

B

E

E

A

A

Time in Risk Bands

PROCrypto Risk · Analyze the distribution of time spent in different risk ban...

B

B

E

E

A

A

Price By Risk Level

PROCrypto Risk · Calculate and display predicted cryptocurrency prices at dif...

B

B

E

E

A

A

Alpha (Momentum/Deviation)

PROCrypto Analysis · Analyze cryptocurrency momentum and deviation from long-term...

B

B

E

E

A

A

KAMA Moving Average

PROCrypto Analysis · Cryptocurrency price analysis with Kaufman Adaptive Moving A...

B

B

E

E

A

A

Cryptocurrency Market Breadth

PROCrypto Analysis · Analyze market participation by tracking how many cryptocurr...

B

B

E

E

A

A

Altcoin Season Index

PROCrypto Analysis · Track altcoin vs Bitcoin performance cycles by measuring the...

B

B

E

E

A

A

Combined VWAP MVRV Z-Score

PROCrypto Analysis · Multi-asset Z-Score indicator that aggregates VWAP MVRV Z-Sc...

B

B

E

E

A

A

Fear & Greed Index

Crypto Analysis · Track market sentiment with the Bitcoin Fear and Greed Index...

B

B

E

E

A

A

Advanced Decline Index

PROCrypto Analysis · Track market breadth using Advanced Decline Index (ADI)

B

B

E

E

A

A

Price Horizons

Crypto Analysis · Displays price across four time horizons (Days, Months, Year...

B

B

E

E

A

A

ROI Analysis

Crypto Analysis · Return on investment analysis across different market segmen...

B

B

E

E

A

A

Sharpe Ratio Analysis

Crypto Analysis · Analyze risk-adjusted returns using the Sharpe ratio to meas...

B

B

E

E

A

A

RSI

Crypto Analysis · Analyze cryptocurrency market using RSI Analysis - the Relat...

B

B

E

E

A

A

Economic Indicators vs Crypto Correlation

Crypto Analysis · Analyze the rolling correlation between various economic ind...

B

B

E

E

A

A

Global M2 vs Crypto Correlation

Crypto Analysis · Analyze the rolling correlation between Global M2 Money Supp...

B

B

E

E

A

A

Moving Averages

Crypto Analysis · Analyze price trends using multiple moving averages to ident...

B

B

E

E

A

A

Bitcoin Fractal Dimension

Crypto Analysis · Analyze market complexity using fractal dimension calculatio...

B

B

E

E

A

A

Power Law Model

Crypto Analysis · Bitcoin price model based on the power law relationship P(t)...

B

B

E

E

A

A

GoldWave

Crypto Analysis · Advanced trend analysis using SMMA-based wave indicators to ...

B

B

E

E

A

A

Death Cross Analysis

Crypto Analysis · Track Death Cross events (50D MA crossing below 200D MA) and...

B

B

E

E

A

A

Crypto Volume Analysis

Crypto Analysis · Analyze cryptocurrency trading volume alongside price action...

B

B

E

E

A

A

Monthly Returns Table

Crypto Analysis · View Bitcoin's historical monthly returns in a comprehensive...

B

B

E

E

A

A

Days Since Percentage Decline

Crypto Analysis · Tracks the number of days since Bitcoin experienced a specif...

B

B

E

E

A

A

Price Derivative

Crypto Analysis · Plots the first derivative (rate of change) over time, showi...

B

B

E

E

A

A

Crypto Relative Strength

Crypto Analysis · Compare the relative strength and performance between two cr...

B

B

E

E

A

A

Annualized Volatility

Crypto Analysis · Measure cryptocurrency price volatility using a rolling wind...

B

B

E

E

A

A

968 charts

↑↓navigate↵selectescclose⌘Qtoggle